WHY INVEST IN A VENTURE CAPITAL FUND-OF-FUNDS

September 2022

Authors: Salman Farmanfarmaian and Richard Rimer

TL;DR

Venture Capital (VC) funds have consistently outperformed the market.

Top-tier VCs have outperformed the markets by A LOT.

Top-tier VCs have a high chance of remaining top-tier in their successor fund.

Industry data provides strong support for a multi-vintage approach to VC investments, concentrated on top-tier VC funds.

key findings

The analysis below distills some of the key findings apparent in both academic and industry studies on VC, notably:

i) a series of papers written by University of Chicago’s Steven Kaplan (together with other academics at Wharton and Oxford), based on data from more than 1,400 VC funds, with vintages starting in 1984 (‘the Kaplan studies’)[1] , and;

ii) industry reports and analysis from Cambridge Associates (‘CA’), the industry reference for VC fund performance, which has surveyed more than 2,000 VC funds since 1995.

Our key findings can be summarised across the following four areas:

Performance – Venture funds have beaten the public markets consistently.

Dispersion – The best Venture funds perform extraordinarily well, but the rest don’t. In other words, if you don’t invest with the best Venture funds, you’ll probably underperform the market.

Persistence – The best Venture funds have a high probability of continuing to be the best. The best VC funds are difficult to access (scarcity), but accessing them is a winning strategy.

Concentrated Diversification – Even the best Venture funds can have weaker vintages given the idiosyncratic nature of venture…or just because they find themselves overpaying during boom cycles. Diversification across vintages and a core set of managers (combined with industry-insider knowledge) is a tangible benefit that a Venture Capital fund-of-funds (FoF) can deliver.

PERFORMANCE

Venture capital funds have consistently outperformance the markets.

The chart below shows the performance of Venture Capital (VC) funds over various periods versus a public market benchmark (mPME).[2] As we can see, overall, VC funds have beaten the public markets quite consistently. However, the average data belies a deeper truth which is that average VC (out)performance is driven by a very small subset of Venture funds – namely the top-quartile of managers.

DISPERSION

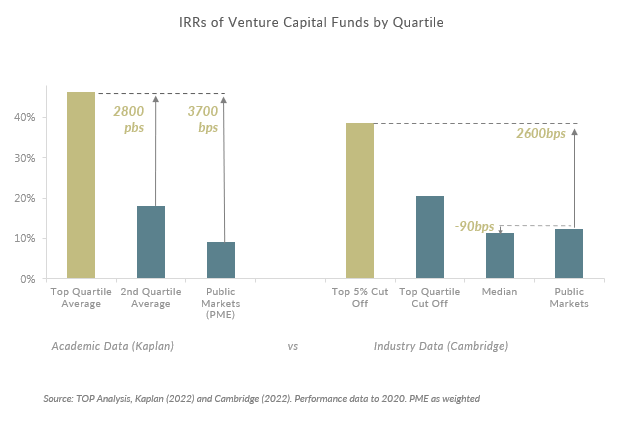

The best venture capital funds have outperformed the markets by a lot.

Indeed, both academic and industry data indicate that Venture funds demonstrate particularly high dispersion – that is: the difference between the best performing VC funds and the rest is enormous.

For example, the Kaplan studies show that top-quartile Venture managers generated a 46% IRR – that is, 2,800bps better than the average of the 2nd quartile managers, and 3,700bps better (or 5x higher) than the public comparable. Similarly, the CA data shows that top-quartile and top-5% VC funds outperformed public markets annually by at least 800bps, and 2,600bps respectively, where median VC funds underperformed by around 90bps.

What’s more CA shows that for the industry’s worst vintages of 1999, 2000 and 2001, the minimum return for a top-5% Venture fund was 16%, 12% and 19% respectively. That is the worst(!) performance ever of the best VC funds(!), and it compares to the median of the industry which generated returns of -3%, -1% and 0.7%, during those same years. Even in those post-bubble years, the best VC Funds generated returns more than 2x the public benchmark PME (of 2.2%, 5.3% and 6.8%).

It is also enlightening to compare dispersion in Venture Capital to other investment classes. As seen in the chart below, managers in other investment classes experience far less dispersion than Venture funds.

This means that there is far more to gain (or lose) when selecting which Venture managers to back. Investors accustomed to selecting managers across other asset classes need to take a very different tack when investing in Venture Capital.

PERSISTENCE

Data suggests that the best venture capital funds have a high chance of continuing to outperform the markets by a lot.

So how do you select the best Venture funds to invest in? Obviously, you must understand the strategy, pick the managers carefully, and do your due diligence. This is difficult and requires specialist knowledge. However even without this expertise, you could have a winning strategy: Data reveals that VC funds demonstrate a phenomenon called persistence. VC funds that have outperformed in the past tend to outperform in their subsequent funds. A top-quartile VC has a 45% probability of being top-quartile in their subsequent vintage – this is almost 2x the probability of landing in the top-quartile if the VC fund was to be chosen randomly.

This increased probability of outperforming likely strengthens the more top-quartile funds a manager has delivered in the past. The venture business benefits from a flywheel effect. Entrepreneurs typically want to be backed by the best Venture Capital managers because they believe these managers have the strongest brands and can add the most value. Often these entrepreneurs are former executives of companies that have been backed by the Venture fund, and so the connections are made naturally. Thus, top-tier Venture funds stand first in line to back the entrepreneurs with the greatest probability of success… and this regardless of where the start-up is based. This ‘unfair’ advantage supports the Venture funds’ likelihood to outperform, and once again attract the next generation of era-defining entrepreneurs. This flywheel effect builds on itself and is difficult to break.

So – as we’ve seen - in Venture Capital, success begets success, and investors can reasonably expect outperformance if they allocate to funds that have consistently outperformed in the past. Easy enough!?... the problem is that there is a lot of demand for investing in the top-tier Venture funds but nowhere near enough capacity. Top-tier managers typically size their fund based on the number of proven investment GP’s (a number which doesn’t scale!), while at the same time, existing investors seek to double-down on these winning VC’s. This is why the best VC funds are heavily access-constrained. N.B. This is particularly true in times of market uncertainty where there is a powerful flight to quality. The result is that premier VCs rarely take on new investors.

To access these proven funds, it is not only your relationships that matter, but the trust and credibility that underpins that relationship…and has been built over multiple cycles. Venture funds want investors who deeply understand their business, share their philosophy and vision, and can add value without getting in the way.

CONCENTRATED DIVERSIFICATION

Industry data provides strong support for a multi-vintage approach to VC investments, concentrated on top-tier funds.

Venture funds are also aware that they are in a high-risk, high-return business. The best funds know the bulk of their portfolio companies will fail, while a handful of fund-returners will drive performance. As can be seen in the chart below (and depending on market cycles as well as the imponderables of an investment partnership), it is always possible that a single fund (managed by a top-tier brand) has less than its share of super-returners, and that its performance suffers. This is where diversification becomes key.

The analysis below uses a Monte Carlo simulation based on the CA data to show the probability of outperformance when investing in Venture funds. The dotted red line shows that choosing any individual fund to invest in at random has a 50%+ chance of underperformance. Allocating to a randomly selected basket of Venture funds (dashed beige line) allows for a lower probability of underperformance, but the average return barely beats the market.

What’s interesting is that when we integrate Kaplan’s findings into the analysis and assume that the FoF invests only in Venture funds that have been top-quartile in their previous vintage, this not only boosts annual performance by 600Bps, but it also ensures a 97.4% probability that the FoF will beat the market.

It is therefore critical for investors to allocate to Venture as a program, i.e., diversified across various top-tier managers, and vintages. Given the capital outlays required (in the order of a couple hundred million dollars every 2-3 years), it is outside the reach of most investors to build such a Venture Capital program on their own. A multi-vintage FoF is a great way to be part of such a Venture program.

In selecting a multi-vintage FoF, it is also important that the FoF remain highly concentrated around a core set of top-quartile managers. Allocating a material portion of the fund to emerging/unproven managers will likely dilute returns and wipe out the FoF’s ability to outperform.

A FoF which follows the precepts delineated above will ensure consistent outperformance over time.

CONCLUSION

Based on both academic & industry research, the above insight demonstrates that a multi-vintage FoF made up of a concentrated portfolio of best-in-class Venture managers is an efficient way for an individual or a small institution to build a Venture program which can deliver net outperformance over time.

References

[1] Main academic sources of data are papers written by Steven Kaplan from the University of Chicago together with colleagues from Oxford (Said) and Virginia (Darden), notably: Harris R., Jenkinson T, Kaplan S. and Stucke R. Has Persistence Persisted in Private Equity? Evidence from Buyout and Venture Capital Funds, SSRN id2304808, March 2022 (‘the Kaplan studies’ or ‘Kaplan et al.’).

[2] The PME (or mPME) is constructed based on the underlying public market index as adjusted to reflect the cashflows and compounding effects of a closed-end structure.

Disclaimer

The content of this article has been approved and issued by TOP Fund Advisors SA for information purposes only and does not purport to be full or complete. The information and opinions contained in this document are for background information and discussion purposes only and do not purport to be full or complete. No information in this document should be construed as providing financial, investment or other professional advice.